California Tax

Why Is My S-Corp Costing More Than $800 in California?

“Why am I paying more than $800 a month for my S-corp?” is one of the most common questions we hear from business owners in their first year after making the election — and the first thing to clear up is that the $800 was never a monthly number. It's annual. If something is hitting your bank account every month, it isn't the state franchise tax — it's one of several other costs that come bundled with running an S-corp, and almost nobody explains them together in one place. Let's fix that.

The $800 itself: what it actually is

California taxes S-corps at the greater of 1.5% of net income or $800 per year. That $800 is the minimum franchise tax — the floor. If your S-corp made $10,000 in net income, you'd still owe $800, because 1.5% of $10,000 is only $150. If your S-corp made $200,000 in net income, you'd owe $3,000 (1.5% of $200,000), not $800, because the percentage tax has overtaken the floor.

This is filed on California Form 100S, due the 15th day of the third month after your tax year ends — March 15 for a calendar-year S-corp. One state return, once a year, for a number that scales with profit.

The part almost nobody tells you: year one might cost $0

California has a permanent rule (Revenue & Taxation Code § 23153) exempting a newly formed or newly qualified corporation — including an S-corp — from the $800 minimum in its first taxable year. You still owe 1.5% on any actual net income in that first year, but if there's no minimum tax floor, a break-even or loss year can genuinely cost $0 in state franchise tax.

This exemption does not apply to LLCs. If you're coming from an LLC, this is the one place the entity type actually changes your bill — not the S-corp election itself.

Until January 1, 2024, LLCs had a similar first-year break under a temporary law (AB 85). That law expired. Every California LLC formed since then owes the $800 starting in year one, no exceptions. Corporations — S-corps included — never lost this break; it isn't tied to AB 85 at all and has no scheduled expiration.

The real break-even number: $53,333

Since the tax is the greater of 1.5% of net income or $800, there's a specific profit level where the percentage catches up to the floor: $800 ÷ 1.5% = $53,333. Below that in net income, you're paying the $800 minimum regardless. Above it, your state tax bill grows with your profit — roughly $1.50 for every additional $100 of net income.

For most of our clients — side-hustle owners who've grown into S-corp territory, typically north of $80,000–$100,000 in profit — this means the state tax is somewhere between $1,200 and $3,000+ a year, not $800. That's still real money, but it's dwarfed by the self-employment tax savings the S-corp election is generating in the first place.

If you're coming from an LLC, the comparison isn't what you think

A California LLC taxed as a partnership or disregarded entity pays the $800 annual tax plus a separate LLC fee based on gross receipts — not profit, revenue:

- $0 below $250,000 in California-source gross receipts

- $900 at $250,000–$499,999

- $2,500 at $500,000–$999,999

- $6,000 at $1,000,000–$4,999,999

- $11,790 at $5,000,000 and up

Electing S-corp tax treatment moves you out of this fee schedule entirely — you're taxed under the $800-or-1.5%-of-profit rule instead, with no gross receipts fee at all. For a service business with thin margins and high revenue, this alone can make the S-corp election cheaper at the state level, independent of any payroll tax savings. It's a genuinely different answer depending on whether your LLC fee, at your revenue, is bigger or smaller than what 1.5% of your profit would be.

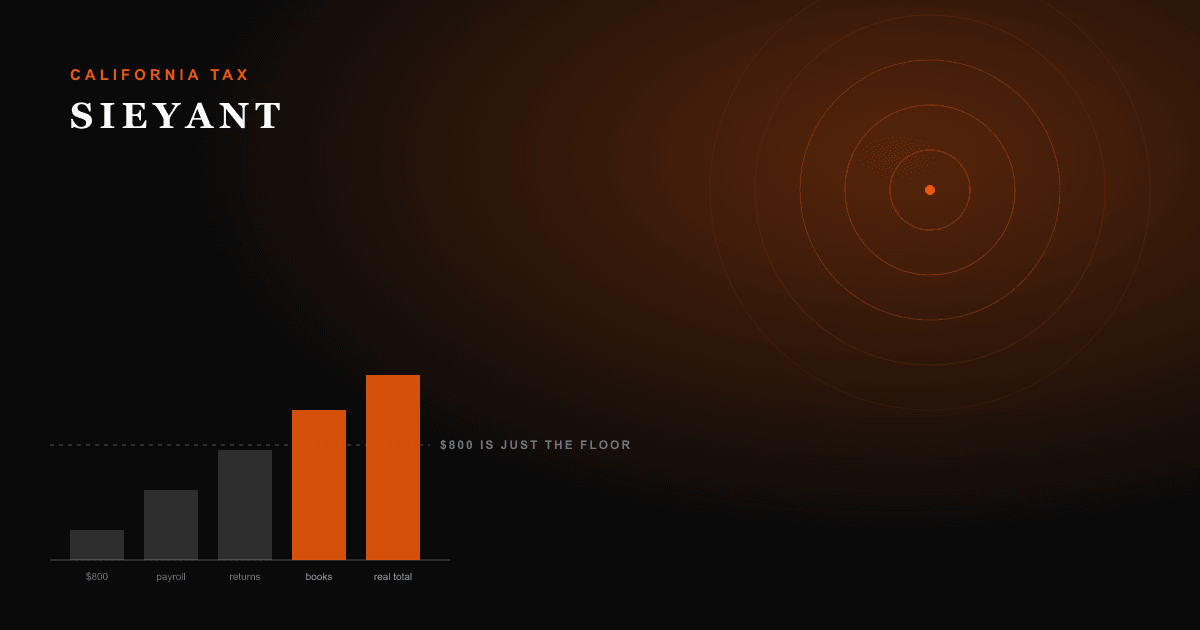

So where's the “more than $800” actually coming from?

Almost always, it's not the franchise tax. It's the operating costs that come with the S-corp structure itself:

- Payroll processing — an S-corp requires you to run actual payroll for yourself, with withholding, quarterly payroll tax filings, and W-2s. A payroll service typically runs $40–$100+ a month, whether you have one employee or ten.

- Two tax returns instead of one — a federal 1120-S and a California 100S, both separate from your personal 1040. Preparation cost is generally higher than a Schedule C.

- Bookkeeping that actually holds up — the IRS expects your salary to be “reasonable” for the work you do, and reasonable is a documented, defensible number, not a guess. That requires clean books, not a shoebox of receipts in March.

- Payroll tax administration — federal and state withholding deposits, unemployment insurance, and the associated filings, on a schedule the IRS sets, not you.

Add it up and a modest S-corp — profit in the $80,000–$150,000 range — is realistically looking at somewhere around $2,500–$5,000 a year in state tax, payroll processing, and return preparation combined. That's the honest “more than $800” number. For the right profit level, it's still meaningfully less than the self-employment tax the election is saving — but it should never be a surprise, and it should never be sold to you as “just $800.”

The number that actually matters isn't the franchise tax in isolation — it's the franchise tax plus the operating cost, compared against what you're saving on self-employment tax. Below roughly $60,000–$80,000 in consistent profit, that comparison usually doesn't favor the S-corp yet. Above it, it usually does. Worth running the actual numbers before either assuming it's a bargain or assuming it isn't.

The information provided on this site is for general informational purposes only and does not constitute tax, legal, or financial advice. Every situation is different — consult a qualified professional regarding your specific circumstances before making any financial or tax decisions.