Tax Strategy

LLC → S-Corp vs. Corporation → S-Corp: Do You Actually Need to Convert Your Entity?

One of the most persistent misconceptions in small business tax planning is that “becoming an S-corp” means dissolving your LLC and forming a brand-new corporation. It doesn't. S-corp is a federal tax election — a choice about how the IRS taxes your business — not a legal entity type you register with the state. What actually happens next depends entirely on what you're starting from.

Starting from a corporation: the simple case

If you've already incorporated, your business is by default taxed as a C-corp — profits taxed at the entity level, then taxed again as dividends when distributed to you. Electing S-corp status here is genuinely simple: file Form 2553 with the IRS, get all shareholders to consent, and meet the eligibility rules (100 or fewer shareholders, one class of stock, only eligible shareholders like individuals and certain trusts, no nonresident alien owners). Nothing about the legal entity changes. One form, and your existing corporation is now taxed as a pass-through instead of being taxed twice.

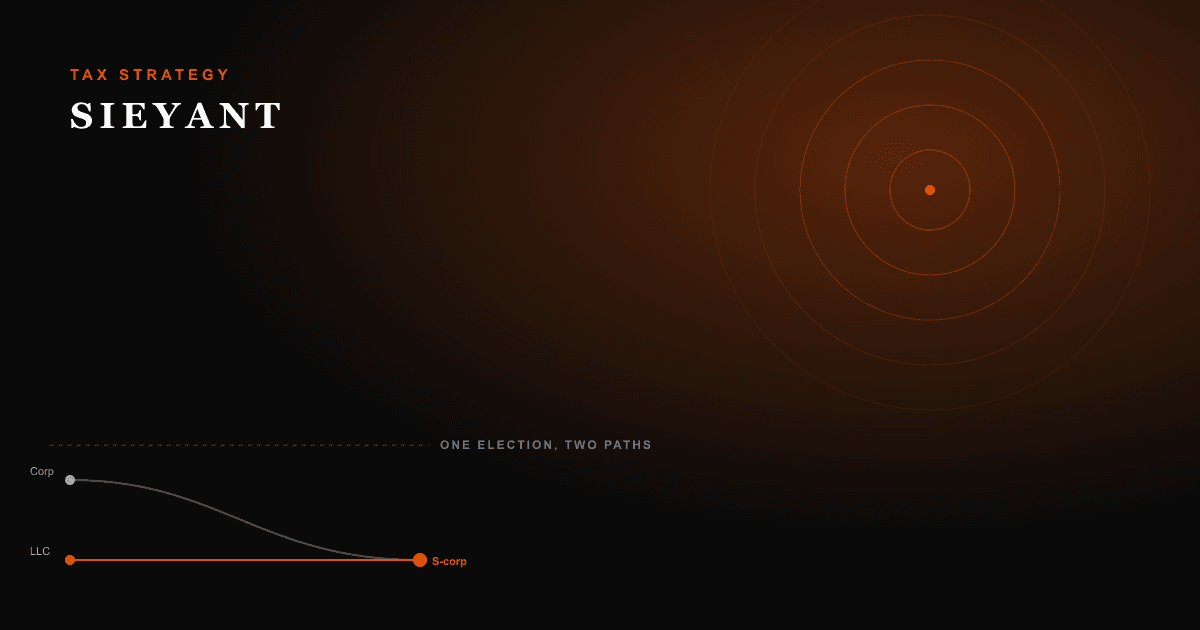

Starting from an LLC: more common, more misunderstood

Most of our clients come from this side. The good news: an LLC doesn't need to convert into a corporation first. Per the IRS instructions for Form 2553, an eligible LLC that timely files Form 2553 is treated as having simultaneously elected to be classified as a corporation for tax purposes and elected S-corp status — both in one filing. You don't need to separately file Form 8832 (the entity classification election) first, though some preparers file it alongside Form 2553 anyway, purely as extra documentation in case the IRS questions the election later.

Your LLC keeps its name, its state registration, its liability protection, and its operating agreement. Only the way its profit is taxed changes.

There's one real catch, and it's the part most LLC operating agreements get wrong for this purpose: the “one class of stock” rule. The IRS treats this as requiring that profit and loss be allocated strictly in proportion to ownership percentage — no special allocations, no different treatment for different classes of membership interest. Plenty of LLC operating agreements do include special allocations, because LLCs are allowed that flexibility by default. If yours does, that language needs to be reviewed and typically amended before or when you make the election — otherwise you risk an invalid S-corp election down the line.

The deadline is the same either way

Regardless of starting point, Form 2553 is generally due within 2 months and 15 days of the start of the tax year you want the election to apply to — March 15 for a calendar-year business that's already operating. Miss it, and you're generally waiting until the following year, though the IRS does offer late-election relief (Rev. Proc. 2013-30) for reasonable-cause situations, which comes up often for LLCs that operated all year as if they'd already made the election and simply missed the paperwork.

What actually changes, and what doesn't

- Doesn't change: your legal entity type, your name with the Secretary of State, your liability protection, your EIN.

- Doesn't change: for an LLC, your operating agreement's core structure — aside from the pro-rata distribution requirement above.

- Changes: how the IRS taxes your profit — splitting it into a reasonable salary (subject to payroll tax) and distributions (not subject to self-employment tax).

- Changes: your filing requirements — you now run payroll and file a separate business return (Form 1120-S), regardless of whether you started as an LLC or a corporation.

- Changes (California specifically): the state generally accepts your federal S-corp election automatically, and — if you were an LLC — moves you off the LLC gross receipts fee schedule and onto the $800-or-1.5%-of-net-income corporate franchise tax rule.

The election itself is the same one-page form no matter where you're starting from. What differs is what needs to be checked and cleaned up beforehand — shareholder eligibility for a corporation, operating agreement language for an LLC — and that's the part worth having someone actually review before you file, not after.

The information provided on this site is for general informational purposes only and does not constitute tax, legal, or financial advice. Every situation is different — consult a qualified professional regarding your specific circumstances before making any financial or tax decisions.